Buying your first home with a partner, spouse or colleague is an exciting milestone, however, it also comes with its share of challenges. The home-buying process for most isn’t always sunshine and rainbows. It can be accompanied by some complicated, sometimes heated, however necessary conversations. Understanding that not everything may go to plan is important and communication is key. At the end of the day, with someone by your side, it’s all worth it when you both find the perfect home for you.

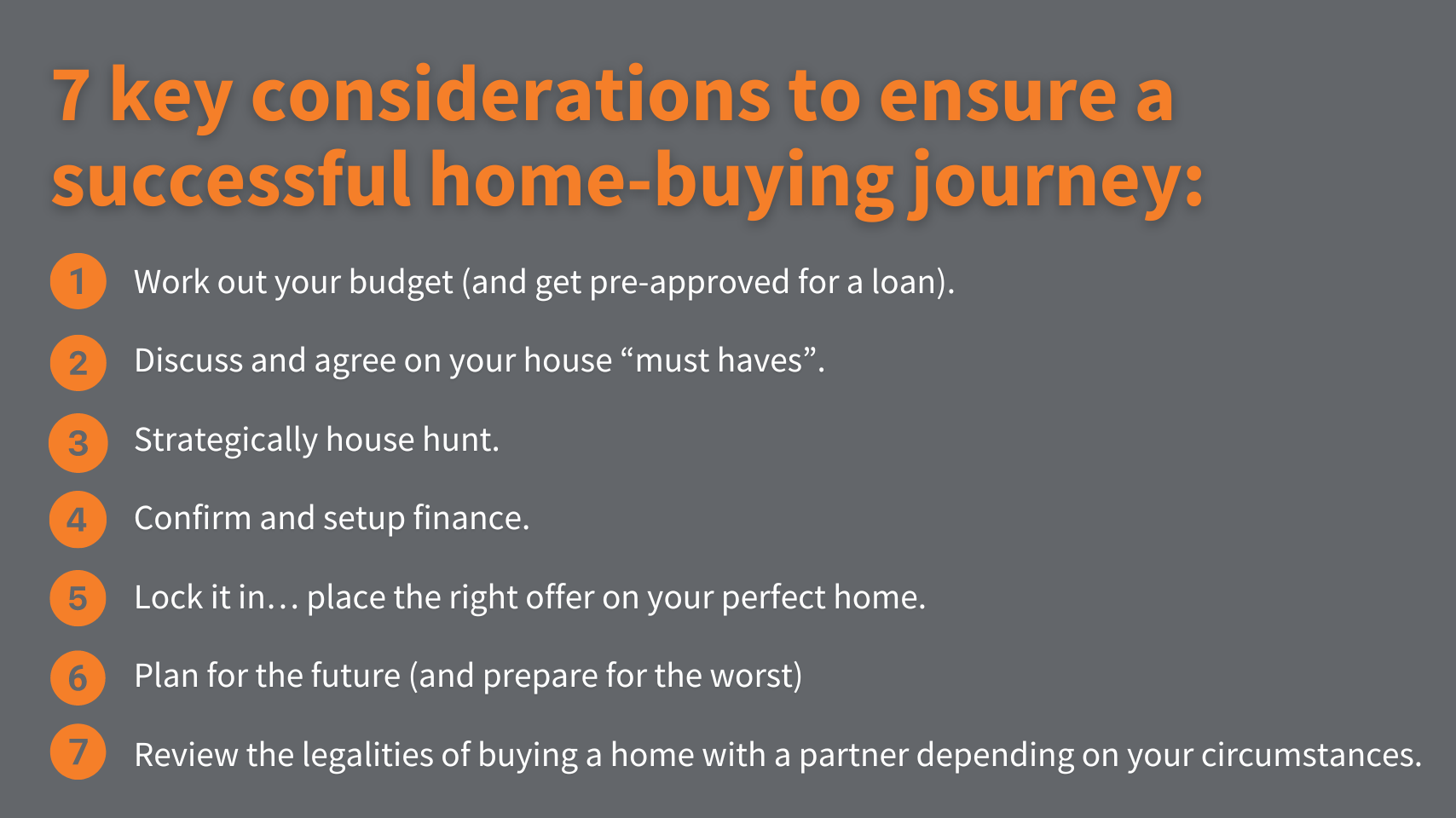

Here are seven key considerations to ensure a successful home-buying journey:

1. Work out your budget (and get pre-approved for a loan).

Before you start the endless search for a home it’s best to know what is realistic for you both in terms of the budget for a home. Things that are important in this discussion include:

- How much deposit have you saved?

- How much are you able to borrow from the bank and under what conditions?

- Can you utilise any government initiatives like the First Home Owner’s Grant?

Think about the budget that will still allow you to have a life but also meets your wants and needs of a house. A common rule is to ensure mortgage repayments don’t surpass

28-30% of your take-home pay.

And don’t forget about all the hidden extras that come along with the process such as loan fees, insurance, stamp duty etc. Help from a professional can be helpful with this aspect of the process. Either an accountant or financial advisor can plan and structure your budget so that it suits your life and the outcomes you want.

This budget phase is also a good time to try and get pre-approved for a home loan. This step will allow you to have a better idea of how much exactly you can loan from the bank but will also help you when you are making offers on houses. Pre-approval makes you a stronger candidate in the mix of offers that might be placed on one house.

2. Discuss and agree on your house “must haves”.

Now that the groundwork is done, the next step to discuss what you both “must have” in the property. During this stage, it is also important to have discussions around what house attributes are necessary and what features you are happy to compromise on. Being on the same page before you start to go for house inspections is critical. Some questions that might help with this process include:

- What locations or areas would we be happy living in?

- How far from work, transport, shops can it be?

- How many bedrooms, bathrooms etc. do we need?

- Do we want something modern that requires little to no renovation or are we happy to renovate and spend time to update a house?

- Is it fine if we buy something smaller and upsize down the track if needed?

- What are some deal breakers?

- Is it for investment or our forever home?

Engaging a real estate agent is also a great idea as they can help you find houses on the market that are within your budget and also meet your needs. Agents bring a wealth of knowledge and understanding of the property market’s current state and can provide helpful professional advice to help inform your decisions.

3. Strategically house hunt

It’s time to get serious…this calls for strategic house hunting. Depending on the area you are looking to buy in, competition can often be intense. In some metro city areas and surrounding suburbs, finding a home or an apartment that satisfies both your needs and budget can be challenging. Attending Open Homes, searching the web for online listings and making offers can be a very time-consuming process.

Good news though! There are many things you can do to help make the process smoother and easier, such as, setting up notification alerts on real estate apps and websites and contacting a local real estate agent to register your interest in suitable listings that become available in the market. These little tips will help you save valuable time and energy on what seems like an endless search sometimes.

When going for house inspections, take notes, photos and videos. Talk about the pros and cons and workarounds.

Once you have both looked at a few, start comparing them and discussing your favourites and why. These discussions all help to develop a better idea of what you really like, hopefully this makes the search much easier!

4. Confirm and setup finance.

Before you make the final step of buying a home together, you will need to figure out what loan type you will apply for and whether it will be under one person’s name or both. Will it be a fixed, variable, or split loan? They all come with their individual pros and cons and interest rates.

Home ownership is usually set up as either joint tenants with equal 50% ownership or tenants in common where the percentage of ownership is based on the amount of money you contribute. It is important to note that lenders will usually consider each individual’s financial situation and creditworthiness when starting a joint loan application.

5. Lock it in… place the right offer on the home you want

You’ve found the one… how lucky! Time to make the final plunge and make an offer. Either you are buying at auction, or it will be a private treaty sale.

A private treaty can sometimes prove difficult when trying to decide what to offer. Some things to think about is if the asking price of the home is fair and how much are you willing to offer. If there is quite a lot of competition and you have capacity to, you might want to offer a more competitive bid that is higher than the asking price.

If buying at an auction be sure to agree on a purchase limit and stick to it. Preparation for auctions is key, study up on the house and really make sure that it is definitely the property that meets both of your expectations. This preparation will also help you keep a level head as auctions can become stressful. Ensure you have your finances in order because generally the deposit of a house up for auction is due on the day. So, if you do win the auction battle be prepared to hand over the deposit, which typically is 10% of the sale.

6. Plan for the future (and prepare for the worst!)

As we all know, unexpected things happen, partnerships can break. It might not be the fun part of the home buying process but thinking ahead is just as important. The following factors are essential to think about and discuss; protecting your assets, what will happen if you cannot make mortgage repayments due to separation, redundancy, job loss etc.

For unmarried couples it is especially important to address potential issues that could arise in the future. This discussion might result in acquiring more insurance and/or putting everything in writing in a co-purchase agreement in case of separation. If you decide to get a co-ownership agreement, you should always seek advice from a professional who can ensure both parties are protected if you part ways in the future.

In case of an emergency such as job loss or an illness, a common tactic buyers may adopt is to set up an emergency fund where in case of something happening, they can still make their mortgage repayments and other necessary bills. Partners will typically try to have two-to-six months’ worth of mortgage repayments ready in a savings account. This just acts as a lifeline to alleviate the money stress that comes with home ownership and unexpected emergencies.

7. Review the legalities of buying a home with a partner depending on your circumstances.

In Australia, it is common to have de facto relationships where a couple is planning on buying a house but are not married. This process comes with a couple of extra legalities to consider. There are variances from state to state but in general, de facto couples are entitled to the same rights as a married couple when buying a home. A couple that has been in a committed, long-term relationship together can then decide if they want to do a joint tenancy or tenants in common agreement. This would also be the same for couples who are not in a romantic relationship, such as family or friends.

It is still important to consider the structure of ownership and any future implications that could arise and cause challenges.

These include:

- Mortgage repayments

- How to split income and costs associated with the property

- When to sell

- When to refinance

- What happens in the case of a relationship breakup

Reaching out to a professional to gain legal advice and to create a co-ownership agreement can help with the items mentioned above and provide more clarity around the legal side of buying and owning a home with a partner.

The team at bytherules Conveyancing are always ready to help with all your conveyancing, speak to our friendly staff on 1300223344 or fill out an enquiry form and we will get back to you.